This is the Ride AI newsletter: The most comprehensive digest of news and intelligence at the intersection of technology and transportation.

Today we're debuting Ground Truth, a new series from Ride AI that focuses on the entrepreneurs and executives building the infrastructure layer for scaling autonomous vehicles. For our inaugural edition, we're introducing you all to Aseon Labs, which launched out of stealth this week.

To suggest candidates for us to feature in Ground Truth or to get in touch about partnership opportunities for the series, please drop me a note at mike@rideai.org. I'd love to talk to more builders, the more esoteric and unsexy the problem, the better.

Introducing Aseon Labs

Few people in a room are more gregarious than George Kalligeros and Dan Keene, especially when you get them talking about robotaxi economics. “Vehicles are autonomous on the road but the moment they need servicing,” says Kalligeros. “Everything becomes manual again — and that's where scale breaks.”

Kalligeros and Keene, who previously built Pushme into the world's largest battery-swapping network before its 2020 acquisition by TIER, are building what they call “robotic pitstop infrastructure”: modular pods that let AV fleets charge, clean, and reset without ever leaving their service zones. Ride AI caught up with the Aseon founders this week as they unveiled their ambitions to the world for a wide ranging conversation on rightsizing the robotaxi business model, the policy risk of empty AVs on streets and why the best infrastructure is invisible to the end user.

Let's get right into the product to start. Describe what Aseon Labs is actually building. What does a pod do, physically and operationally?

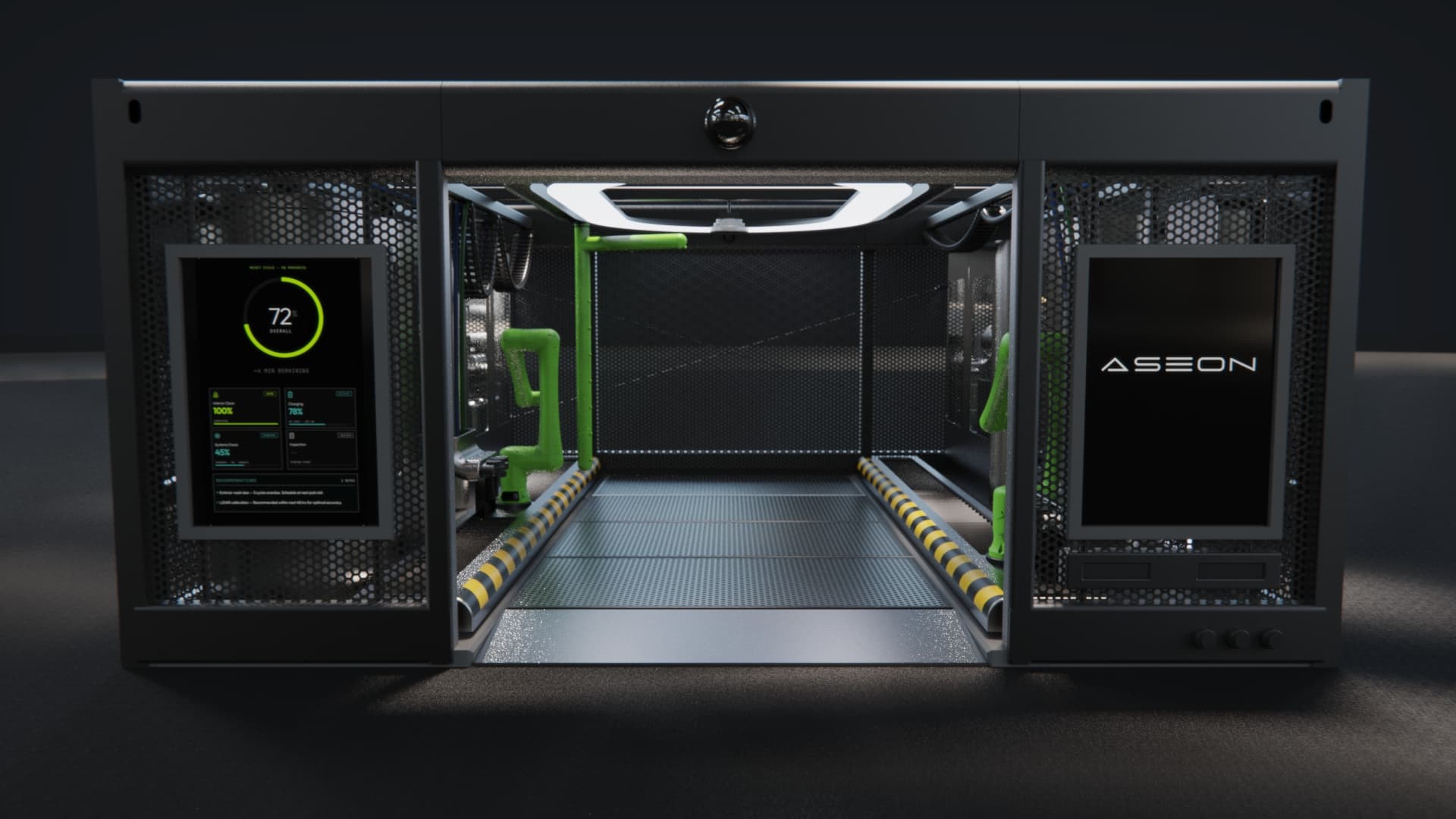

At Aseon, we build robotic pitstop infrastructure for autonomous vehicle fleets.

Today, robotaxis still rely on centralized depots for charging, cleaning, inspection and routine servicing. We think that architecture becomes a major bottleneck as fleets scale. Vehicles spend too much time deadheading to depots, waiting in queues and sitting offline during revenue-generating hours.

Our product is essentially a “depot in a box” — a compact robotic station deployed directly inside operating zones. Physically, the pod combines charging, interior cleaning, sensor cleaning, visual inspection and other repetitive servicing workflows into a small-footprint automated system. Operationally, it allows fleets to perform high-frequency resets much closer to demand.

One of the key insights for us was that the overwhelming majority of robotaxi resets are operationally predictable. Most vehicles do not require deep servicing or human intervention. They require the same repeatable workflows, performed consistently, many times per day.

We therefore designed the pod around a simple principle: replicate the behavior of a human depot operator as closely as possible, but do it robotically, continuously and in distributed urban locations.

To this point, you've been building in stealth. What did that period allow you to do and why now to showcase what you're building to the world?

The stealth period was less about building in isolation and more about pressure-testing the operating assumptions behind AV infrastructure.

We spent time inside depots across multiple US cities studying how fleets actually operate today: where time is lost, how labor is structured, how charging queues form, and how real estate constraints shape deployment decisions.

In parallel, we modelled different levels of distributed servicing penetration across fleets to understand where the economics inflect. What became very clear is that proximity to reset capacity matters enormously. The closer servicing moves toward demand, the lower the deadhead mileage and the higher the effective fleet utilization.

We also realized the problem is as much physical infrastructure and permitting as it is robotics. Large depots are slow to permit, difficult to scale and increasingly constrained by urban real estate availability. But once you reduce the servicing footprint dramatically, an entirely different class of urban locations becomes viable.

We decided to come out of stealth now because we want to drive the conversation around micro-depots and distributed AV infrastructure. We think the industry is still largely thinking in terms of centralized fleet operations, while the long-term operating model for autonomy will look much more distributed and embedded throughout the city.

So in a sense, this is partly a real estate play — co-locating pods on underutilized urban infrastructure like parking lots and EV charging networks. How does that commercial relationship work, and why would a Volterra or similar operator want to do this deal?

In many ways, autonomous infrastructure becomes a real estate optimization problem.

Once you compress depot workflows into a footprint closer to one or two parking bays, a much broader set of urban infrastructure becomes economically useful. Existing charging sites, parking assets, fuel retail and underutilized commercial land all become potential nodes in a distributed AV servicing network.

For charging operators, the proposition is straightforward: AV fleets create highly predictable, recurring energy demand. Most public fast charging infrastructure today still suffers from inconsistent utilization. Robotaxi fleets change that dynamic entirely because they operate continuously and can commit forecastable throughput under long-term agreements.

More broadly, we think the market shifts from building a handful of massive depots toward orchestrating a dense network of smaller operational nodes across the city.

The economic argument for autonomous vehicles is largely a pure utilitarian one. These vehicles should theoretically run for far more hours than a human driver can. How badly does the current maintenance overhead dent that thesis?

The core economic promise of autonomy is utilization. A robotaxi should theoretically generate revenue far more hours per day than a human-driven vehicle.

But today, a surprising amount of operational time is still lost to servicing logistics. Vehicles routinely travel long distances to centralized depots, spend meaningful time offline during resets, and often perform these workflows during active demand windows rather than true downtime periods.

Public California data already shows how significant the inefficiency is: a very large percentage of AV miles are still driven empty.

What matters operationally is compressing two things simultaneously:

- distance to servicing

- servicing cycle time

The industry has already become very good at vehicle autonomy. The next challenge is operational autonomy — designing infrastructure systems that keep vehicles continuously active inside the city rather than constantly pulling them back toward centralized depots.

Walk me further through what the maintenance cycle actually looks like for a robotaxi fleet today. How many hours and miles are being lost?

It varies significantly by operator and city topology, but the broad pattern is surprisingly consistent.

A vehicle typically leaves the operating zone multiple times per day to return to a centralized depot for charging, cleaning and inspection. The actual depot turnaround may only take around an hour gate-to-gate, but once you include travel time to and from the depot, the vehicle can easily spend close to two hours out of service per reset cycle.

The important point is that many of these resets occur during periods when the vehicle could otherwise be generating revenue. So the cost is not just labor or energy — it's lost utilization.

When you combine deadhead miles, downtime, labor and infrastructure overhead, reset costs quickly become economically material at fleet scale — in some cases approaching the amount of revenue a vehicle may generate in a full day.

When we chatted at Ride AI 2026, you mentioned that the most successful infrastructure in history shares one trait: it disappears. What does “disappeared” actually look like for AV service infrastructure — how do you know when you've reached that threshold?

The best infrastructure eventually becomes invisible to the end user.

People do not actively think about cellular towers, data centers or electrical substations during daily life, even though modern cities depend on them completely. We think AV servicing infrastructure evolves similarly.

As autonomous fleets scale, vehicles will continuously require charging, cleaning, inspection and temporary parking somewhere inside the urban environment. The question is whether those operations happen through highly visible centralized facilities, or quietly through distributed infrastructure embedded throughout the city.

Our view is that the long-term winner is infrastructure that minimizes operational friction while remaining largely invisible to the public realm.

You previously scaled Pushme to 5,000 locations across 40 markets. How much of that playbook applies here, and what's genuinely different about this problem?

A surprising amount of the Pushme playbook applies here.

At Pushme, we learned that scaling physical infrastructure in cities depends less on technical elegance and more on deployment simplicity. Infrastructure needs to be non-intrusive, fast to deploy, operationally lightweight, and create a very clear incentive for the site host. That is what makes distributed infrastructure scalable, because you are dealing with a very large number of unique smaller sites.

We also learned that distributed infrastructure scales far faster than centralized infrastructure because it can piggyback on existing urban assets rather than requiring purpose-built facilities.

Aseon applies many of the same principles, just at a different operational scale. Our pods are designed to deploy quickly, integrate into existing parking and charging environments, and transform small pieces of urban real estate into productive AV operational capacity.

Deploying physical infrastructure in cities means dealing with permitting, zoning, and various layers of municipal rigamarole. What does the policy complexity look like specifically for your pods, and how do you navigate it?

Permitting and land use are absolutely central to the problem.

One of the reasons traditional depots become difficult to scale is that large-footprint automotive infrastructure triggers increasingly complex zoning, traffic and environmental review processes in dense urban areas.

Our approach is to minimize infrastructure intensity as much as possible. The smaller and more modular the deployment footprint becomes, the easier it is to integrate into existing commercial parking, charging and mobility environments rather than requiring entirely new industrial development.

In practice, we spend a significant amount of time thinking about how pods interact with existing land use categories, utility access, traffic flow and curbside dynamics. The robotics matter, but deployment velocity matters equally.

Cities are increasingly noticing empty robotaxis crossing their streets with no passengers. How much of the problem you're solving is economic, and how much of it is actually a public perception and political problem that the industry hasn't fully acknowledged?

A meaningful part of the challenge is absolutely political and perceptual, not just economic.

Cities will tolerate autonomous vehicles at scale only if they improve urban efficiency rather than simply adding more empty miles and curbside congestion.

Today, a substantial amount of AV movement still happens without passengers — whether for resets, repositioning or demand balancing. Some of that inefficiency is inevitable during early deployment phases, but long term the industry has to reduce unnecessary vehicle movement dramatically.

We think distributed servicing infrastructure plays an important role here. The closer operational capacity moves toward demand, the less vehicles need to circulate empty through cities simply to remain operational. At the same time, infrastructure like Aseon can also help fleets stage vehicles safely off-street between rides rather than continuously circulating through the urban environment.

Where does the category go from here? What does the infrastructure layer for a fully scaled AV city look like in a decade? Said another way, who else should I talk to for this series that Ride AI readers may not know about?

We're already seeing the early shift away from purely centralized fleet operations toward more distributed and automated infrastructure models.

Charging is moving closer to operating zones, servicing workflows are becoming increasingly modularized, and fleets are experimenting with smaller operational footprints throughout cities rather than relying exclusively on massive depots.

Long term, we think autonomous vehicles will require an entirely new infrastructure layer optimized around continuous utilization. Not just charging infrastructure, but operational infrastructure — systems that keep fleets active, maintained and staged close to demand.

What interests us most is the interaction between vehicles, energy and urban real estate. Cities are effectively becoming operating systems for autonomy, and the allocation of physical space becomes strategically important.

There are several thoughtful operators already working on adjacent parts of this stack. We particularly respect the work Ming Maa and the team are doing around distributed AV fleet operations and infrastructure orchestration.

Get the latest AV news delivered to your inbox

This article was originally published on Ride AI's Substack.

← Back to News